List of IFSC Code, MICR Code, and Addresses of all Banks in India

IFSC Codes By Popular Banks

SBI New Delhi IFSC Code

Bank: SBI Bank (State Bank of India)

IFSC Code: SBIN0001537

MICR Code: 110002022

Branch: Connaught Place

District: New Delhi

State: Delhi

Address: B 37 By 38, Second Floor, Inner Circle Connaught Circus, New Delhi

ICICI Karnataka IFSC Code

Bank: ICICI Bank

IFSC Code: ICIC0006561

MICR Code: 560229057

Branch: Bangalore M.G. Road

District: Bangalore

State: Karnataka

Address: 11-C, Mittal Towers, M.G. Road, Bangalore, Karnataka

Axis Maharastra IFSC Code

Bank: AXIS Bank

IFSC Code: UTIB0000373

MICR Code: 400211033

Branch: Goregaon (East)

District: Greater Mumbai

State: Maharashtra

Address: Manish Chambers, Commercial Complex CTS. 87/A, Sonawala Road

HDFC West Bengal IFSC Code

Bank: HDFC Bank

IFSC Code: HDFC0001015

MICR Code: 700240038

Branch: Dalhousie

District: Kolkata

State: West Bengal

Address: Jardine House – 4, Clive Row, Kolkata

- SBI

- Bank of Baroda

- Axis Bank

- ICICI Bank

- Indian Bank

- Canara Bank

- Bank of India

- HDFC Bank

IFSC Codes in India

What is an IFSC Code?

IFSC is an acronym for Indian Financial System Code. IFSC code is a unique eleven-digit number which is a combination of alphabets and numerals. It is used to transfer funds online for NEFT, IMPS and RTGS transactions. Usually, the IFSC code can be found on the cheque-book provided by the bank. It can also be found on the front page of the accountholder’s passbook. The IFSC code of each bank branch is assigned by the Reserve Bank of India. The account holders can easily check the IFSC code of their bank/branch on the Reserve Bank of India’s website. Internet banking transactions for transferring funds, using NEFT, IMPS and RTGS, can’t be initiated without a valid Indian Financial System Code.

Generally, there isn’t any change or update in the 11-digit IFSC code. Recently, the State Bank of India changed Indian Financial System Code of its branches all over the nation after the merger with five associate banks and 1 other bank.

The Importance of IFSC code

The points mentioned below highlight the importance of IFSC code.

- Unique Identification- It helps in identifying a particular bank branch

- Elimination Errors It helps to eliminate any discrepancy in the fund transfer process.

- Electronic Payments Made Easier- It used in electronic payment tools such as RTGS, IMPS, and NEFT.

The format for Bank IFSC Code

The first 4 characters of IFSC code are alphabets which represent the bank. The fifth character is zero (0). Usually, the last 6 characters are numbers but they can be alphabets as well and represent the bank branch.

| A | B | C | D | 0 | 1 | 2 | 3 | 4 | 5 | 6 |

| Bank Code | 0 | Branch Code | ||||||||

How does IFSC CODE work?

Electronic funds transfer in India is facilitated by an alpha-numeric code called the Indian Financial System Code (IFS Code or IFSC). This code exclusively recognizes each bank branch which participates in the two main settlement and payment systems in India, namely, National Electronic Funds Transfer (NEFT) and Real Time Gross Settlement (RTGS).

IFSC code is an eleven-character code that is assigned by the Reserve Bank of India (RBI). The first portion of the code is composed of four letters representing the bank. Next character is zero that is reserved for future use. The last 6 characters are the identification code of the branch.

Let’s take an example:

IFSC Code of State Bank of India (SBI) starts with letters ‘SBI’. As there are a lot of banks with several branches, the IFSC code is used to identify the branch involved in the transaction.

IFSC codes are vital while carrying out payment transactions including RTGS, NEFT transfers. Like, for SBI, the IFSC Code will be SBIN0011569 for the branch located in Sector 31, Gurugram.

Modes of Online Money Transfer Using IFSC Code (Detailed Info About NEFT, RTGS, IMPS)

There is no denying the fact that almost everyone in our circle is dependent on online payment modes and most certainly, you too are no exception. This online trend is supported by a plethora of options – thanks to the digitization of monetary transactions.

The convenience of transferring funds online has certainly made our lives much easier. Almost, every other bank provides multiple payment options such as Immediate Payment Service (IMPS), National Electronic Funds Transfer (NEFT), Real Time Gross Settlement (RTGS), etc.

Based on different parameters, such as the speed of transfer, the transaction value, service availability, etc. each of the above-stated payment transfer methods will offer a diverse range of features and flexibility. Although these payment methods have their own set of benefits, yet they come with their varied flexibility and convenience for the customers.

How can IFSC code help you Transfer your Money Through NEFT?

National Electronic Fund Transfer (NEFT) is one of the most widespread online methods of transferring funds from one bank to another. NEFT is based on a deferred arrangement which actually means that the money is transferred in different sets (batches).

Currently, there are 12 payment settlements sets arranged between the time slab of 8 am and 7 pm for weekdays (Monday to Friday) and six payment settlements between 8 am and 1 pm for Saturdays.

Although there isn’t any cap on the amount that one can transfer through NEFT, however, a few banks have put a limit. For instance, SBI (State Bank of India) has put a cap of Rs 10 lakhs for NEFT transfer amount under their retail banking option.

Step-by-step procedure to transfer money via NEFT:

- To start with, your bank branch should be NEFT-enabled. You can visit RBI’s (Reserve Bank of India) website to check and confirm so.

- Complete the registration process for your net banking account by creating a username and password. However, your mobile number should be registered with your bank to complete the net banking registration.

- Afterward, you need to add the beneficiary to your account to whom you want to transfer the money. To do this, you will need the beneficiary’s name, her/his bank account number and the IFSC (Indian Financial System Code) of her/his bank branch. IFSC can be either found on the bank statement or on the cheque leaf.

- Once you have successfully added the beneficiary, there might be a waiting time (assigned by the bank) before you can transfer funds to the added beneficiary. Again, for instance, SBI has a waiting time of 4 hours.

- Once logged into your net banking account, go to the option of ‘Transfer Funds’, select the name of the particular beneficiary you want to transfer funds to and complete the transfer with the help of an OTP (One Time Password) sent to your registered mobile number.

- The amount will be transferred to the beneficiary as per the next settlement’s schedule.

The NEFT costs between Rs 2.50 to Rs 25 (+ service tax), depending on the amount transferred to the beneficiary.

There are also certain limitations of NEFT transactions like you cannot transfer funds at any time you feel doing so. This service is available only on working days and within the working hours of your bank. You won’t be able to avail this service on weekends and bank holidays.

The RTGS Option (Real Time Gross Settlement)

- RTGS transfer is basically meant for high-value funds transactions. The minimum amount that can be transferred through RTGS is Rs 2 lakhs. There isn’t any cap on maximum transfer. As this transfer takes place on a real-time basis, the individual to whom the amount is being transferred to will receive the amount in approximately 30 minutes.

- The RTGS service works from 9 am to 4:30 pm on weekdays and 9 am to 2 pm on Saturdays.

- The procedure to use RTGS service is same as NEFT. You simply need to make sure that your, as well as the beneficiary’s, bank accounts are RTGS-enabled and you have the IFSC code of his/her bank branch.

- RTGS is a bit costlier than NEFT, wherein a transfer of Rs 2- Rs 5 lakhs may cost you a fee of Rs 30, whereas the transactions above Rs 5 lakhs may cost you Rs 55.

The Immediate Payment Service (IMPS)

- IMPS is an instant fund service and works 24*7. It can be used 365 days a year to transfer funds to any other bank account. This service was introduced in 2010 by National Payments Corporation of India.

- You don’t have to register separately for IMPS service – once you are logged into your net banking account, you will get the option of transferring your funds either by NEFT, RTGS or IMPS. You can choose the IMPS option to carry out the transfer.

- Once again, you will need the beneficiary’s full name, her/his bank account number and IFSC code to complete the transfer. In case you transferring funds through the mobile app of your bank, you would also need MMID (Mobile Money Identifier) code for IMPS.

- MMID is a 7-digit number issued by the bank for IMPS service if the individual is using mobile banking as a beneficiary. Also, while conducting IMPS through mobile, there isn’t any need of the beneficiary to get registered.

- The charges for using IMPS is decided by the banks. However, usually the charge for fund transfer up to Rs 1 lakh is Rs 5 and for a transfer between Rs 1-2 lakhs is up to Rs 15.

What is the use of IFSC?

An IFSC code is used by the Indian financial system to facilitate an online and electronic transfer of money. It is the IFSC code of a bank which enables it to help people with NEFT and RTGs.

IFSC Code Pattern

In an IFSC code, the first four characters are alphabets which denote the bank name. Hence, the IFSC code of each branch of the same bank will begin with the same four letters. The fifth character is zero.

The remaining six characters are digits or numbers which denote the branch code. This is the part which makes an IFSC code unique.

How to know the IFSC Code?

It is simple. If you have an account with any branch of any bank, you will automatically get to know its IFSC code as it is printed on the passbook.

However, if you want to know the code without creating an account, you can do so via the internet. There is an official website of IFSC code where you can know all about this code.

What Is a MICR Code?

MICR is an acronym for Magnetic Ink Character Recognition. Primarily, this innovative technology authenticates the legality and credibility of paper-based document(s) in the banking database. It can be found on cheques. MICR is at par with IFSC as far as the security of a fund transfer is concerned.

MICR code is a product of highly advanced Character Recognition Technology (CRT) used by banks to verify cheques for clearance. MICR technology is used for other bank documents as well. A MICR code is placed at the bottom of a cheque. It includes details such as the bank code, account details, amount, and cheque number, alongside a control indicator. The biggest advantage of MICR technology is that it stands out among similar concepts, such as barcodes, as MICR can be read and distinguished by humans very easily.

Difference between IFSC Code & MICR Code

As monetary transactions are not limited to financial institutions like banks, thorough verification is necessary before processing a transaction. To make the process faster, simpler and automatic, banks and other financial institutions rely on certain codes. These codes, namely, MICR Code and IFSC Code, play a significant role in verifying the authenticity of a transaction. However, there is a difference between the usage of both these codes.

Let’s gather a clear understanding of both and learn how they differ from each other-

| IFSC Code | MICR Code |

| It is used to facilitate electronic money transfer between the banks in India. | MICR code is initiated to make cheque processing simpler and faster. |

| IFSC Code is an 11-digit alpha-numeric code | MICR is a 9-digit code |

| The first four characters indicate the name of the bank. | The first three digits represent the city code where the bank branch is located. |

| Last 6 digits represent the bank location | Last three digits indicate the bank branch code. |

How to search for the IFSC Code of a particular Bank’s Branch

Abbreviated as Indian Financial System Code, IFSC is an 11-digit alphanumeric code that is used to identify the bank branches that participate in various electronic monetary transactions like NEFT or RTGS. One can find the IFSC code either in his/her bank passbook or on the chequebook. The image below can help you understand better.

One can search for the IFSC Code of any bank branch by visiting the official website of a particular bank or by calling on their helpline number. For instance, if you want to know HDFC bank South Delhi branch code:

- You can call the branch over the phone and ask the IFSC Code

- As said before, you can find it on the chequebook or passbook given by the bank

- You can find IFSC codes on RBI’s official website as well. It is mentioned with the list of banks participating in the RTGS/NEFT network

- Apart from the above, third-party websites like PolicyBazaar.com also helps you find the required information. To get the IFSC code of HDFC Bank, visit HDFC bank IFSC code page of PolicyBazaar.com. Click on the tab ‘Search HDFC Bank code by Branch’. Make the relevant selection by clicking on the drop-down menu and enter the required details like state, district, branch. Once you submit this information, the entire details of that particular bank branch will appear in front of you.

How can one Transfer Money with IFSC Code of the Bank?

With IFSC Code, online money transfer has become easier and hassle-free. RBI has assigned these codes to the bank branches to perform NEFT, RTGS and IMPS fund transfer in a smooth way. To know how IFSC Code works while transferring money, let’s take an example here. The IFSC code of HDFC Saket, New Delhi branch is HDFC0000043.

- Here, the first four digits identify the bank, which is HDFC Bank.

- The 5th digit is always ‘Zero’.

- The remaining 6 characters 000043, helps Reserve Banks of India (RBI) identify the branch of the bank

Let’s know how IFSC Code works during a transaction. When a fund transfer is initiated, one has to provide the bank account number and the IFSC code of the payee. Once the remitter provides all the necessary information, the fund is transferred to the account of the beneficiary with the help of IFSC Code in a smooth way. Fund transfer with IFSC code takes only a few minutes from the time of initiation.

IFSC Code also can be used at the time of purchasing mutual funds or insurance through NetBanking. As the National Clearing Cell of Reserve Bank of India monitors all transactions, IFSC Code helps RBI to keep a track of various transactions and execute fund transfer without any hassle.

How to e-transfer Fund?

Nowadays, most of the people opt for some or the other online process to transfer fund from one account to another. The process of e-transfer of funds is not only simple but it is also hassle-free. Moreover, it saves you from the trouble of going to the bank and standing in a queue to transfer funds. You just need to follow a few simple steps to successfully transfer your money from one account to another. Let’s take a look at these step.

- First and foremost, in order to avail the online services offered by your bank, it is important that you get yourself registered for the bank’s net banking services.

- You will need to register the recipient account as a beneficiary for third-party transactions. (Note that, beneficiary refers to the third party from a different bank than yours)

- You will be required to add the beneficiary account and the recipient bank branch’s IFSC code.

Process of Registering a Third Party Beneficiary:

Majorly, every bank in India has its own policy regarding a third-party fund transfer. However, the method of third-party fund transfer remains more or less the same for every bank, except they are presented a bit differently.

Let’s take a look at the process to register a third party beneficiary.

- Enter your customer ID and PIN and log-in to the online banking service of the bank.

- Click on ‘fund transfer’ option. You will be directed to a new page.

- Go to request tab, you will see an option to add a beneficiary. Click on that option.

- Enter the recipient’s account details:

- Name of Beneficiary

- Account number

- Beneficiary Bank’s IFSC Code.

- Bank Branch

- After filling all these details, click on ‘submit’ button.

- Once the registration is complete, it takes a certain amount of time for the service to activate. Once done, you can then transfer funds.

- After the beneficiary is added to your account, you will have to enter the description and amount that you want to transfer to the beneficiary’s account.

- Once you are done with that, select the option of communication detail i.e. either mobile or email.

- Based on whatever option you choose, you will receive an OTP either on your registered mobile number or on the email ID.

- After the verification of OTP is completed, your fund will be transferred to the beneficiary account.

Different Methods of Fund Transfer with the Help of IFSC Code

The online process of fund transfer with the help of IFSC code is not that difficult as it seems. To the contrary, it is simpler and hassle-free. While processing fund transfer from one account to another, IFSC code is key information that facilitates the transfer. However, there are different methods of transferring funds with the help of IFSC code. Let’s take a look at these methods.

Through App:

Almost every smartphone has apps these days. You can make the most of your bank’s apps available in google play/app store. Moreover, you can also initiate fund transfer through an app. Here are few basic steps that you need to follow in order to transfer fund through a particular bank app.

- First and foremost, you need to have an activated net banking system for your account.

- Download the net banking app of your bank.

- Open the app; enter the login PIN or credentials, like the customer ID and password to open your account.

- Choose the option of fund transfer; you will see various options of third-party fund transfer like:

- Between My Accounts

- Within Bank

- Instant Transfer to Other Bank-IMPS

- To Other Bank- NEFT

- Via Visa Card

- Via Special Payment

- Choose the NEFT option of fund transfer.

- In case, you have not added the beneficiary, then first them by entering the name of the beneficiary, bank account number, and the IFSC code of the respective bank branch.

- Once you completed the process of registration, it will take around 5 mins- 12hrs to activate the beneficiary account for money transfer. This time period to link the accounts generally depends upon the bank policy.

- Once the beneficiary account is linked to your account, you can easily initiate an instant money transfer to the beneficiary’s account.

Through SMS:

You can also transfer money through the SMS process with the help of an IFSC code. Let’s take a look at how you can transfer fund through SMS.

- To transfer money through the process of SMS, first, you will need to link your mobile number to your bank account by registering your phone number for mobile banking.

- In order to register, you will be required to fill a form, after which a starter’s kit will be sent to you which will include a unique 7 digit number i.e. MMID and mPin.

- Once you get yourself registered, you will be required to create an SMS and type IMPS along with the beneficiary details like beneficiary name, account number, IFSC code of the beneficiary bank and the sum amount you want to transfer.

- Once you confirm the transaction, you will receive a confirmation message wherein you will have to enter your mPin.

- Press ok after entering the mPin, and the fund will be transferred to the beneficiary account.

So, with these methods, you can easily transfer funds to the beneficiary account with the help of an IFSC code.

What is UPI?

An RBI regulated entity, National Payment Corporation of India (NPCI), has developed an instant payment system known as the Unified Payment Interface (UPI). UPI operates over IMPS infrastructure and allows instant transfer of money between any two bank accounts. In case you are registering with the service for the first time, you’ll need to create a 4 to 6-digit UPI Pin (Personal Identification Number). You will have to enter the UPI PIN to perform all UPI transactions. UPI payment method allows fund transfer offline and online. Moreover, irrespective of the bank’s working hours, an individual can instantly transfer funds anytime.

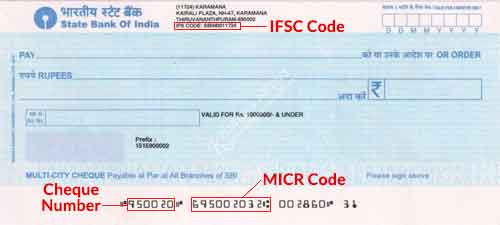

Locate IFSC Code and MICR Code on a Bank Cheque

What is IFSC code and how to locate it on a cheque?

Definition: IFSC (Indian Financial System Code) is an 11-digit alphanumeric code that helps to identify different bank branches that deal with online fund transfers either via NEFT (National Electronic Funds Transfer), IMPS (Immediate Payment Service) or RTGS (Real Time Gross Settlement).

The starting 4 digits of the IFSC signify the bank’s name, followed by a 0 (the 5th digit) and the last 6 digits stand for the branch of a particular bank.

You can also find the IFSC code on the top of a cheque leaf near the bank account number.

What is MICR how to locate it on a cheque?

Definition: MICR stands for Magnetic Ink Character Recognition and is a 9-digit code that identifies the bank branches that are taking part in an ECS (Electronic Clearing System). MICR code is especially needed if you are filling up different financial forms such as SIP forms, etc. as it helps in a faster clearance of cheques.

The starting 3 digits of the code signify the city code, the next 3 digits (the middle ones) stand for the bank code and the last 3 digits represent the code of the particular branch.

You can easily find the MICR number at the bottom of your cheque leaf, printed adjacent the cheque number (on the right-hand side).

IFSC Codes FAQs

1. What is RTGS code?

Ans. The IFSC code is often referred to as RTGS code or NEFT code, since it is used to transfer money using RTGS.

2. Is IFSC code branch code?

Ans. IFSC code is not the same as branch code. IFSC (Indian Financial System Code) consists of eleven characters and is used to identify the bank and its branch. While the branch code is a part of the IFSC code, it is not the same.

3. What is the meaning of RTGS in banking?

Ans. RTGS stands for Real Time Gross Settlement. RTGS is one of the main payment and settlement systems in India. To make a payment using RTGS, one requires details like name of the account holder, account number and the IFSC code of the bank. Money can be transferred from one bank account to another safely using RTGS. IFSC code is often referred to as RTGS code or NEFT code for the same reason.

4. Is IFSC code and RTGS the same?

Ans. IFSC stands for Indian Financial System Code. The IFSC code comprises eleven characters and is used to identify the bank and its branch. RTGS stands for Real Time Gross Settlement. it is one of two main payment and settlement systems in India. To conduct any such EFT, IFSC is required.

5. What is the branch code of a bank?

Ans. The branch code of a bank branch helps in distinguishing one branch from another. It is available on the bank’s website, printed on cheque books and pass-books. The last 6 characters of any given IFSC code is the branch code.

6. What is the difference between NEFT and RTGS?

Ans. NEFT stands for National Electronic Funds Transfer, whereas RTGS refers to Real Time Gross Settlement. These two are the two main money transferring systems in India. Minimal transfer charges are to be paid for conducting transfers using NEFT or RTGS. The key differences between them are explained below.

| Parameters | RTGS | NEFT |

| Full form | Real Time Gross Settlement | National Electronic Funds Transfer |

| Transfer type | One-on-one settlement | Batches |

| Transfer speed | Nearly Instant | 0-2 hours, settled in batches |

| Minimum transfer amount | Rs 2 lakh | Re. 1 |

| Maximum transfer amount | Rs. 10 lakhs | No limit |

7. Is Cheque required for NEFT?

Ans. No, a cheque is not required for NEFT.

8. Is IMPS faster than NEFT?

Ans. Yes, IMPS is faster than NEFT as the money gets transferred immediately using IMPS while NEFT is settled in time-regulated batches.

9. How much time will it take to settle a NEFT?

Ans. A NEFT is finished immediately. It can sometimes take up to 30 minutes, but it does not take longer than that.

10. Are there any charges for NEFT transfer?

Ans. The charges for NEFT depend upon the slab in which the amount falls. The details of these are given below.

| Transaction slab | Charges |

| Up to Rs. 10,000 | Rs. 2.5 |

| From Rs. 10,000 to Rs. 1 lakh | Rs. 5 |

| From Rs. 1 lakh to Rs. 2 lakh | Rs. 15 |

| From Rs. 2 lakh to Rs. 5 lakh | Rs. 25 |

| From Rs 5 lakh to Rs. 10 lakh | Rs. 50 |

11. Can we stop NEFT payment?

Ans. Once initiated, a NEFT payment cannot be stopped. In case any of the details (account number/ IFSC code) are incorrect, the funds get reversed to the account the payment was initiated from.

12. Can NEFT transfer be reversed?

Ans. A NEFT payment cannot be reversed. However, in case any of the details required (account number/ IFSC code) are entered incorrectly, the funds get reversed to the account the payment was initiated from.

IFSC CODE BY BANK

- SBI

- Bank of Baroda

- Axis Bank

- ICICI Bank

- Indian Bank

- Canara Bank

- Bank of India

- HDFC Bank

- Andhra Bank

- Central Bank of India

- Allahabad Bank

- Punjab National Bank

- Syndicate Bank

- Bank of Maharashtra

- Citi Bank

- UCO Bank

- Dena Bank

- Corporation Bank

- IDBI Bank

- United Bank of India

- Indian Overseas Bank

- Kotak Mahindra Bank

- SBT Bank

- SBM Bank

- Vijaya Bank

- Federal Bank

- Yes Bank

- Indusind Bank

- State Bank of Patiala

- State Bank of Hyderabad